Stocks Rise Led by Japan on Auto Tariff Reprieve: Markets Wrap

In a promising turn of events, global stock markets—particularly in Asia—experienced a surge, led by Japan, following remarks from US President Donald Trump suggesting a possible pause in auto tariffs. This development offers a breath of relief to investors after recent volatility triggered by tariff-related uncertainties and broader trade tensions.

Could Tariff Exemptions Calm Market Volatility?

The recent easing of proposed tariffs on consumer electronics and the possibility of a reprieve in auto tariffs have injected renewed optimism into global markets. With indexes in Japan jumping more than 1%, automakers like Toyota and Honda saw notable gains. This upward momentum helped stabilize trading in China and Hong Kong while aiding recovery in US and European futures.

The move marks a sharp shift from earlier in the month, when reciprocal tariffs imposed by Trump’s administration shaved off nearly $10 trillion from global equities and triggered a sell-off in Treasury bonds.

Tariff Flexibility Provides a Breather

Investors welcomed what appeared to be a more flexible stance from President Trump, helping soothe nerves in an otherwise jittery environment. Yusuke Sakai, a senior trader at T&D Asset Management, noted, "Trump’s showing signs of flexibility around his tariff policies, and that’s brought some composure back to the market."

Nonetheless, markets remain wary as the administration continues to explore tariffs on semiconductor and pharmaceutical imports through Commerce Department-led trade probes. This potential broadening of the trade war underscores the uncertain path ahead.

Currency & Bond Market Reaction

The dollar index has seen a two-week decline, a signal of growing investor concern about the US economy slipping into a recession. In parallel, 10-year Treasury bond yields spiked by 50 basis points last week—marking the sharpest weekly increase in over 20 years.

As inflation expectations climb and the Federal Reserve adjusts its growth outlook, fixed-income markets are signaling caution. Deutsche Bank’s Global CIO Christian Nolting advised a selective strategy, noting opportunities to buy the dip if the S&P 500 drops below 5,000.

Global Equities: Buy the Dip?

"We have also told clients not to panic," Nolting stated on Bloomberg TV, highlighting that there’s still potential growth in the US economy despite elevated uncertainty. This sentiment was echoed by investors willing to re-enter markets if valuations approach recessionary levels.

Luxury and Yen Markets Face Pressures

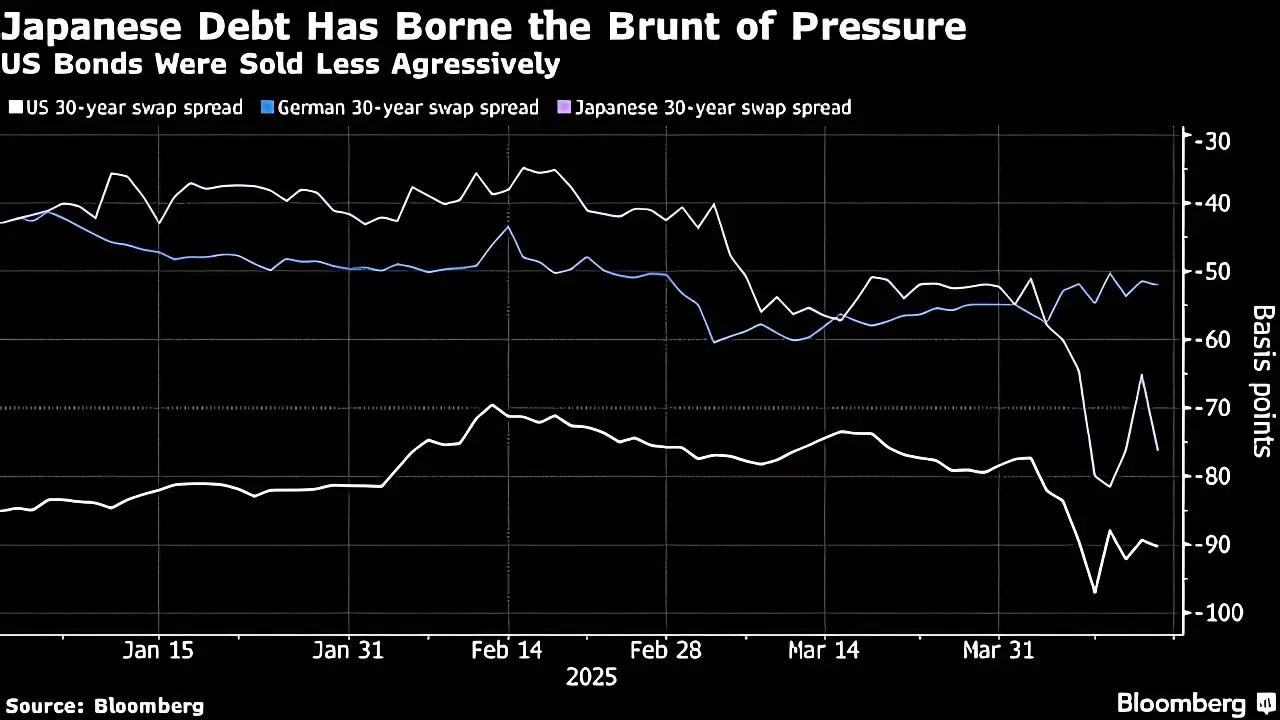

LVMH and other luxury retailers reported softer-than-expected sales, with the drag attributed to declining demand in the US and China. Meanwhile, Japan’s long-term bond yields rose sharply amid speculation of additional fiscal stimulus. The spread between 30-year and 5-year JGBs widened to the highest level in two decades.

This yield surge prompted multiple Japanese firms, including Tepco Power Grid Inc., to postpone yen bond issuances due to heightened volatility.

Bank of Japan's Likely Policy Stance

Given current conditions, analysts believe the Bank of Japan will likely hold off on raising interest rates. A former executive director commented on the prevailing uncertainties that warrant a cautious policy stance.

Christina Woon of Eastspring Investments highlighted the unpredictability stemming from frequent changes in US rhetoric. "The environment that we are in right now is extremely tricky," she said.

US Dollar’s Role at Risk

Bloomberg strategist Garfield Reynold pointed out that the US dollar’s status as the linchpin of the global financial system is under threat. The ongoing trade disputes are diminishing its reputation as a safe haven asset, setting the stage for a potential long-term decline.

China’s Strategic Countermove

Chinese President Xi Jinping’s Southeast Asia tour, which includes visits to Vietnam, Malaysia, and Cambodia, aims to position China as a more stable economic partner in contrast to the US. Still, UBS AG revised down its growth forecast for China to 3.4%, the lowest among major banks, citing tariff-driven export pressures.

Commodities Snapshot

Oil prices saw a modest rebound amid speculation that sanctions on Iranian crude may be relaxed. Meanwhile, gold prices edged closer to record highs, fueled by demand for safe-haven assets.

Market Snapshot

Stocks

-

Japan’s Topix: +1.2%

-

Australia’s S&P/ASX 200: +0.3%

-

Hong Kong’s Hang Seng: +0.2%

-

Shanghai Composite: Little change

-

Euro Stoxx 50 Futures: Little change

-

S&P 500 Futures: -0.1%

Currencies

-

Dollar Index: Slight rebound

-

Euro: $1.1357

-

Yen: 143.02 per dollar

-

Offshore Yuan: 7.3120 per dollar

Cryptocurrencies

-

Bitcoin: $85,220.1 (+0.4%)

-

Ether: $1,633.43 (flat)

Bonds

-

US 10-Year Treasury Yield: -3 basis points to 4.35%

-

Australia 10-Year Yield: -7 basis points to 4.33%

Commodities

-

WTI Crude: +0.4% to $61.75/barrel

-

Gold: +0.6% to $3,228.80/ounce

Conclusion

The global equity markets, led by Japan, have rebounded thanks to potential tariff exemptions from the US. While investor optimism is improving, the environment remains complex, marked by trade uncertainties, fluctuating inflation forecasts, and cautious central banks. Traders and analysts suggest watching key indicators like S&P 500 levels and Treasury yields closely to navigate what remains an unpredictable landscape.